Regression - Forecasting and Predicting

Welcome to part 5 of the Machine Learning with Python tutorial series, currently covering regression. Leading up to this point, we have collected data, modified it a bit, trained a classifier and even tested that classifier. In this part, we're going to use our classifier to actually do some forecasting for us! The code up to this point that we'll use:

import Quandl, math

import numpy as np

import pandas as pd

from sklearn import preprocessing, cross_validation, svm

from sklearn.linear_model import LinearRegression

df = Quandl.get("WIKI/GOOGL")

df = df[['Adj. Open', 'Adj. High', 'Adj. Low', 'Adj. Close', 'Adj. Volume']]

df['HL_PCT'] = (df['Adj. High'] - df['Adj. Low']) / df['Adj. Close'] * 100.0

df['PCT_change'] = (df['Adj. Close'] - df['Adj. Open']) / df['Adj. Open'] * 100.0

df = df[['Adj. Close', 'HL_PCT', 'PCT_change', 'Adj. Volume']]

forecast_col = 'Adj. Close'

df.fillna(value=-99999, inplace=True)

forecast_out = int(math.ceil(0.01 * len(df)))

df['label'] = df[forecast_col].shift(-forecast_out)

X = np.array(df.drop(['label'], 1))

X = preprocessing.scale(X)

X = X[:-forecast_out]

df.dropna(inplace=True)

y = np.array(df['label'])

X_train, X_test, y_train, y_test = cross_validation.train_test_split(X, y, test_size=0.2)

clf = LinearRegression(n_jobs=-1)

clf.fit(X_train, y_train)

confidence = clf.score(X_test, y_test)

print(confidence)

I will stress that creating a linear model with say >95% accuracy is not that great. I certainly wouldn't trade stocks on it. There are still many issues to consider, especially with different companies that have different price trajectories over time. Google really is very linear: Up and to the right. Many companies aren't, so keep this in mind. Now, to forecast out, we need some data. We decided that we're forecasting out 1% of the data, thus we will want to, or at least *can* generate forecasts for each of the final 1% of the dataset. So when can we do this? When would we identify that data? We could call it now, but consider the data we're trying to forecast is not scaled like the training data was. Okay, so then what? Do we just do preprocessing.scale() against the last 1%? The scale method scales based on all of the known data that is fed into it. Ideally, you would scale both the training, testing, AND forecast/predicting data all together. Is this always possible or reasonable? No. If you can do it, you should, however. In our case, right now, we can do it. Our data is small enough and the processing time is low enough, so we'll preprocess and scale the data all at once.

In many cases, you wont be able to do this. Imagine if you were using gigabytes of data to train a classifier. It may take days to train your classifier, you wouldn't want to be doing this every...single...time you wanted to make a prediction. Thus, you may need to either NOT scale anything, or you may scale the data separately. As usual, you will want to test both options and see which is best in your specific case.

With that in mind, let's handle all of the rows from the definition of X onward:

X = np.array(df.drop(['label'], 1)) X = preprocessing.scale(X) X_lately = X[-forecast_out:] X = X[:-forecast_out] df.dropna(inplace=True) y = np.array(df['label']) X_train, X_test, y_train, y_test = cross_validation.train_test_split(X, y, test_size=0.2) clf = LinearRegression(n_jobs=-1) clf.fit(X_train, y_train) confidence = clf.score(X_test, y_test) print(confidence)

Note that first we take all data, preprocess it, and then we split it up. Our X_lately variable contains the most recent features, which we're going to predict against. As you should see so far, defining a classifier, training, and testing was all extremely simple. Predicting is also super easy:

forecast_set = clf.predict(X_lately)

The forecast_set is an array of forecasts, showing that not only could you just seek out a single prediction, but you can seek out many at once. To see what we have thus far:

print(forecast_set, confidence, forecast_out)

[ 745.67829395 737.55633261 736.32921413 717.03929303 718.59047951 731.26376715 737.84381394 751.28161162 756.31775293 756.76751056 763.20185946 764.52651181 760.91320031 768.0072636 766.67038016 763.83749414 761.36173409 760.08514166 770.61581391 774.13939706 768.78733341 775.04458624 771.10782342 765.13955723 773.93369548 766.05507556 765.4984563 763.59630529 770.0057166 777.60915879] 0.956987938167 30

So these are our forecasts out. Now what? Well, you are basically done, but we can work on visualizing this information. So stock prices are daily, for 5 days, and then there are no prices on the weekends. I recognize this fact, but we're going to keep things simple, and plot each forecast as if it is simply 1 day out. If you want to try to work in the weekend gaps (don't forget holidays) go for it, but we'll keep it simple. To start, we'll add a couple new imports:

import datetime import matplotlib.pyplot as plt from matplotlib import style

We import datetime to work with datetime objects, matplotlib's pyplot package for graphing, and style to make our graphs look decent. Let's set a style:

style.use('ggplot')

Next, we're going to add a new column to our dataframe, the forecast column:

df['Forecast'] = np.nan

We set the value as a NaN first, but we'll populate some shortly. We said we're going to just start the forecasts as tomorrow (recall that we predict 10% out into the future, and we saved that last 10% of our data to do this, thus, we can begin immediately predicting since -10% has data that we can predict 10% out and be the next prediction). We need to first grab the last day in the dataframe, and begin assigning each new forecast to a new day. We will start that like so:

last_date = df.iloc[-1].name last_unix = last_date.timestamp() one_day = 86400 next_unix = last_unix + one_day

Now we have the next day we wish to use, and one_day is 86,400 seconds. Now we add the forecast to the existing dataframe:

for i in forecast_set:

next_date = datetime.datetime.fromtimestamp(next_unix)

next_unix += 86400

df.loc[next_date] = [np.nan for _ in range(len(df.columns)-1)]+[i]

So here all we're doing is iterating through the forecast set, taking each forecast and day, and then setting those values in the dataframe (making the future "features" NaNs). The last line's code just simply takes all of the first columns, setting them to NaNs, and then the final column is whatever i is (the forecast in this case). I have chosen to do this one-liner for loop like this so that, if we decide to change up the dataframe and features, the code can still work. All that is left? Graph it!

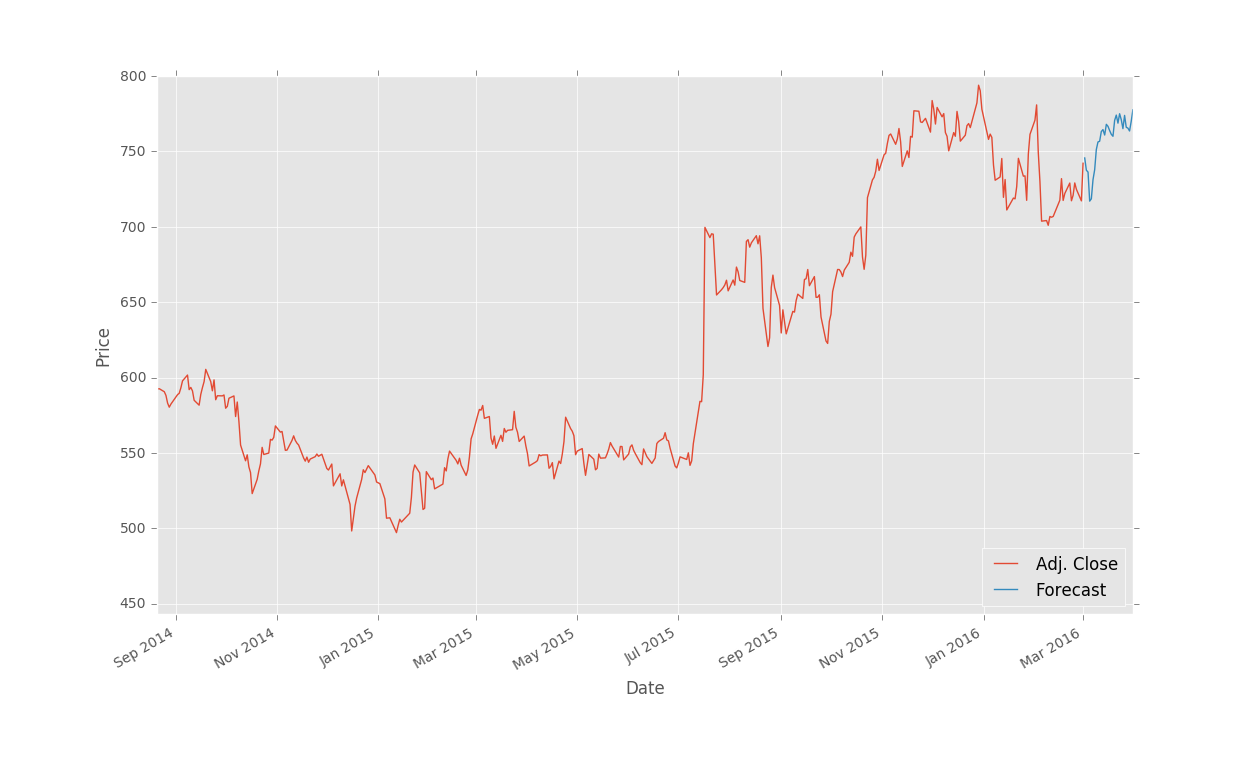

df['Adj. Close'].plot()

df['Forecast'].plot()

plt.legend(loc=4)

plt.xlabel('Date')

plt.ylabel('Price')

plt.show()

Full code up to this point:

import Quandl, math

import numpy as np

import pandas as pd

from sklearn import preprocessing, cross_validation, svm

from sklearn.linear_model import LinearRegression

import matplotlib.pyplot as plt

from matplotlib import style

import datetime

style.use('ggplot')

df = Quandl.get("WIKI/GOOGL")

df = df[['Adj. Open', 'Adj. High', 'Adj. Low', 'Adj. Close', 'Adj. Volume']]

df['HL_PCT'] = (df['Adj. High'] - df['Adj. Low']) / df['Adj. Close'] * 100.0

df['PCT_change'] = (df['Adj. Close'] - df['Adj. Open']) / df['Adj. Open'] * 100.0

df = df[['Adj. Close', 'HL_PCT', 'PCT_change', 'Adj. Volume']]

forecast_col = 'Adj. Close'

df.fillna(value=-99999, inplace=True)

forecast_out = int(math.ceil(0.01 * len(df)))

df['label'] = df[forecast_col].shift(-forecast_out)

X = np.array(df.drop(['label'], 1))

X = preprocessing.scale(X)

X_lately = X[-forecast_out:]

X = X[:-forecast_out]

df.dropna(inplace=True)

y = np.array(df['label'])

X_train, X_test, y_train, y_test = cross_validation.train_test_split(X, y, test_size=0.2)

clf = LinearRegression(n_jobs=-1)

clf.fit(X_train, y_train)

confidence = clf.score(X_test, y_test)

forecast_set = clf.predict(X_lately)

df['Forecast'] = np.nan

last_date = df.iloc[-1].name

last_unix = last_date.timestamp()

one_day = 86400

next_unix = last_unix + one_day

for i in forecast_set:

next_date = datetime.datetime.fromtimestamp(next_unix)

next_unix += 86400

df.loc[next_date] = [np.nan for _ in range(len(df.columns)-1)]+[i]

df['Adj. Close'].plot()

df['Forecast'].plot()

plt.legend(loc=4)

plt.xlabel('Date')

plt.ylabel('Price')

plt.show()

The result (I zoomed in a bit):

There you have it, you now have a somewhat decent method for forecasting stock prices into the future! In the next tutorial, we're going to wrap up regression with some information on saving classifiers as well as using millions of dollars worth of computational power for a few dollars.

-

Practical Machine Learning Tutorial with Python Introduction

-

Regression - Intro and Data

-

Regression - Features and Labels

-

Regression - Training and Testing

-

Regression - Forecasting and Predicting

-

Pickling and Scaling

-

Regression - Theory and how it works

-

Regression - How to program the Best Fit Slope

-

Regression - How to program the Best Fit Line

-

Regression - R Squared and Coefficient of Determination Theory

-

Regression - How to Program R Squared

-

Creating Sample Data for Testing

-

Classification Intro with K Nearest Neighbors

-

Applying K Nearest Neighbors to Data

-

Euclidean Distance theory

-

Creating a K Nearest Neighbors Classifer from scratch

-

Creating a K Nearest Neighbors Classifer from scratch part 2

-

Testing our K Nearest Neighbors classifier

-

Final thoughts on K Nearest Neighbors

-

Support Vector Machine introduction

-

Vector Basics

-

Support Vector Assertions

-

Support Vector Machine Fundamentals

-

Constraint Optimization with Support Vector Machine

-

Beginning SVM from Scratch in Python

-

Support Vector Machine Optimization in Python

-

Support Vector Machine Optimization in Python part 2

-

Visualization and Predicting with our Custom SVM

-

Kernels Introduction

-

Why Kernels

-

Soft Margin Support Vector Machine

-

Kernels, Soft Margin SVM, and Quadratic Programming with Python and CVXOPT

-

Support Vector Machine Parameters

-

Machine Learning - Clustering Introduction

-

Handling Non-Numerical Data for Machine Learning

-

K-Means with Titanic Dataset

-

K-Means from Scratch in Python

-

Finishing K-Means from Scratch in Python

-

Hierarchical Clustering with Mean Shift Introduction

-

Mean Shift applied to Titanic Dataset

-

Mean Shift algorithm from scratch in Python

-

Dynamically Weighted Bandwidth for Mean Shift

-

Introduction to Neural Networks

-

Installing TensorFlow for Deep Learning - OPTIONAL

-

Introduction to Deep Learning with TensorFlow

-

Deep Learning with TensorFlow - Creating the Neural Network Model

-

Deep Learning with TensorFlow - How the Network will run

-

Deep Learning with our own Data

-

Simple Preprocessing Language Data for Deep Learning

-

Training and Testing on our Data for Deep Learning

-

10K samples compared to 1.6 million samples with Deep Learning

-

How to use CUDA and the GPU Version of Tensorflow for Deep Learning

-

Recurrent Neural Network (RNN) basics and the Long Short Term Memory (LSTM) cell

-

RNN w/ LSTM cell example in TensorFlow and Python

-

Convolutional Neural Network (CNN) basics

-

Convolutional Neural Network CNN with TensorFlow tutorial

-

TFLearn - High Level Abstraction Layer for TensorFlow Tutorial

-

Using a 3D Convolutional Neural Network on medical imaging data (CT Scans) for Kaggle

-

Classifying Cats vs Dogs with a Convolutional Neural Network on Kaggle

-

Using a neural network to solve OpenAI's CartPole balancing environment