Basic stock data Manipulation - Python Programming for Finance p.3

Hello and welcome to part 3 of the Python for Finance tutorial series. In this tutorial, we're going to further break down some basic data manipulation and visualizations with our stock data. The starting code that we're going to be using (which was covered in the previous tutorial) is:

import datetime as dt

import matplotlib.pyplot as plt

from matplotlib import style

import pandas as pd

import pandas_datareader.data as web

style.use('ggplot')

df = pd.read_csv('tsla.csv', parse_dates=True, index_col=0)

The Pandas module comes equipped with a bunch of built-in functionality that you can leverage, along with ways to create custom Pandas functions. We'll cover some custom functions later, but, for now, let's do a very common operation to this data: Moving Averages.

The idea of a simple moving average is to take a window of time, and calculate the average price in that window. Then we shift that window over one period, and do it again. In our case, we'll do a 100 day rolling moving average. So this will take the current price, and the prices from the past 99 days, add them up, divide by 100, and there's your current 100-day moving average. Then we move the window over 1 day, and do the same thing again. Doing this in Pandas is as simple as:

df['100ma'] = df['Adj Close'].rolling(window=100).mean()

Doing df['100ma'] allows us to either re-define what comprises an existing column if we had one called '100ma,' or create a new one, which is what we're doing here. We're saying that the df['100ma'] column is equal to being the df['Adj Close'] column with a rolling method applied to it, with a window of 100, and this window is going to be a mean() (average) operation.

Now, we could do:

print(df.head())

Date Open High Low Close Volume \

Date

2010-06-29 2010-06-29 19.000000 25.00 17.540001 23.889999 18766300

2010-06-30 2010-06-30 25.790001 30.42 23.299999 23.830000 17187100

2010-07-01 2010-07-01 25.000000 25.92 20.270000 21.959999 8218800

2010-07-02 2010-07-02 23.000000 23.10 18.709999 19.200001 5139800

2010-07-06 2010-07-06 20.000000 20.00 15.830000 16.110001 6866900

Adj Close 100ma

Date

2010-06-29 23.889999 NaN

2010-06-30 23.830000 NaN

2010-07-01 21.959999 NaN

2010-07-02 19.200001 NaN

2010-07-06 16.110001 NaN

What happened? Under the 100ma column we just see NaN. We chose a 100 moving average, which theoretically requires 100 prior datapoints to compute, so we wont have any data here for the first 100 rows. NaN means "Not a Number." With Pandas, you can decide to do lots of things with missing data, but, for now, let's actually just change the minimum periods parameter:

df['100ma'] = df['Adj Close'].rolling(window=100,min_periods=0).mean() print(df.head())

Date Open High Low Close Volume \

Date

2010-06-29 2010-06-29 19.000000 25.00 17.540001 23.889999 18766300

2010-06-30 2010-06-30 25.790001 30.42 23.299999 23.830000 17187100

2010-07-01 2010-07-01 25.000000 25.92 20.270000 21.959999 8218800

2010-07-02 2010-07-02 23.000000 23.10 18.709999 19.200001 5139800

2010-07-06 2010-07-06 20.000000 20.00 15.830000 16.110001 6866900

Adj Close 100ma

Date

2010-06-29 23.889999 23.889999

2010-06-30 23.830000 23.860000

2010-07-01 21.959999 23.226666

2010-07-02 19.200001 22.220000

2010-07-06 16.110001 20.998000

Alright, that worked, now we want to see it! But we've already seen simple graphs, how about something slightly more complex?

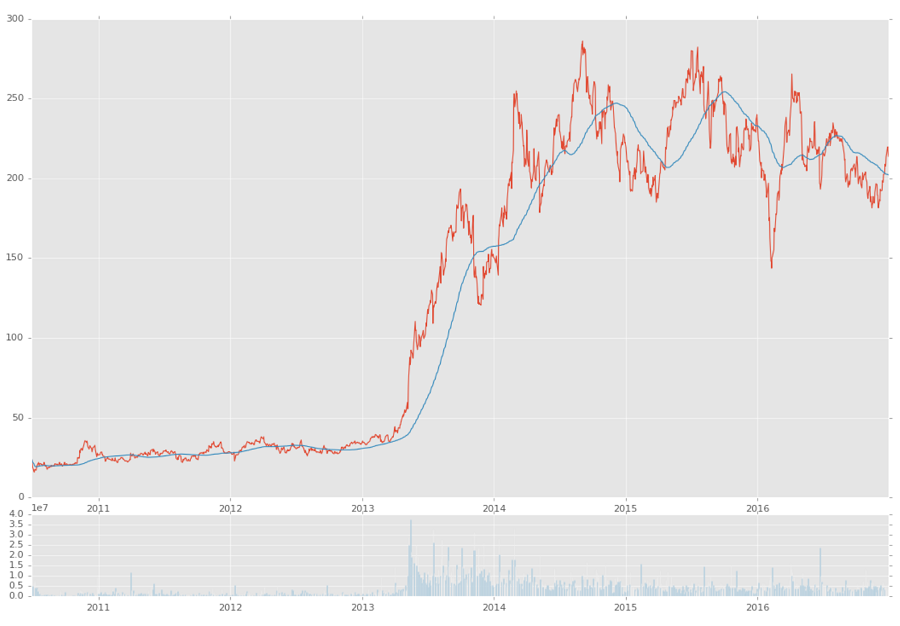

ax1 = plt.subplot2grid((6,1), (0,0), rowspan=5, colspan=1) ax2 = plt.subplot2grid((6,1), (5,0), rowspan=1, colspan=1,sharex=ax1)

If you want to know more about subplot2grid, check out this subplots with Matplotlib tutorial.

Basically, we're saying we want to create two subplots, and both subplots are going to act like they're on a 6x1 grid, where we have 6 rows and 1 column. The first subplot starts at (0,0) on that grid, spans 5 rows, and spans 1 column. The next axis is also on a 6x1 grid, but it starts at (5,0), spans 1 row, and 1 column. The 2nd axis also has the sharex=ax1, which means that ax2 will always align its x axis with whatever ax1's is, and visa-versa. Now we just make our plots:

ax1.plot(df.index, df['Adj Close']) ax1.plot(df.index, df['100ma']) ax2.bar(df.index, df['Volume']) plt.show()

Above, we've graphed the close and the 100ma on the first axis, and the volume on the 2nd axis. Our result:

Full code up to this point:

import datetime as dt

import matplotlib.pyplot as plt

from matplotlib import style

import pandas as pd

import pandas_datareader.data as web

style.use('ggplot')

df = pd.read_csv('tsla.csv', parse_dates=True, index_col=0)

df['100ma'] = df['Adj Close'].rolling(window=100, min_periods=0).mean()

print(df.head())

ax1 = plt.subplot2grid((6,1), (0,0), rowspan=5, colspan=1)

ax2 = plt.subplot2grid((6,1), (5,0), rowspan=1, colspan=1, sharex=ax1)

ax1.plot(df.index, df['Adj Close'])

ax1.plot(df.index, df['100ma'])

ax2.bar(df.index, df['Volume'])

plt.show()

In the next few tutorial, we'll learn how to make a candlestick graph via a Pandas resample of the data, and learn a bit more on working with Matplotlib.

-

Intro and Getting Stock Price Data - Python Programming for Finance p.1

-

Handling Data and Graphing - Python Programming for Finance p.2

-

Basic stock data Manipulation - Python Programming for Finance p.3

-

More stock manipulations - Python Programming for Finance p.4

-

Automating getting the S&P 500 list - Python Programming for Finance p.5

-

Getting all company pricing data in the S&P 500 - Python Programming for Finance p.6

-

Combining all S&P 500 company prices into one DataFrame - Python Programming for Finance p.7

-

Creating massive S&P 500 company correlation table for Relationships - Python Programming for Finance p.8

-

Preprocessing data to prepare for Machine Learning with stock data - Python Programming for Finance p.9

-

Creating targets for machine learning labels - Python Programming for Finance p.10 and 11

-

Machine learning against S&P 500 company prices - Python Programming for Finance p.12

-

Testing trading strategies with Quantopian Introduction - Python Programming for Finance p.13

-

Placing a trade order with Quantopian - Python Programming for Finance p.14

-

Scheduling a function on Quantopian - Python Programming for Finance p.15

-

Quantopian Research Introduction - Python Programming for Finance p.16

-

Quantopian Pipeline - Python Programming for Finance p.17

-

Alphalens on Quantopian - Python Programming for Finance p.18

-

Back testing our Alpha Factor on Quantopian - Python Programming for Finance p.19

-

Analyzing Quantopian strategy back test results with Pyfolio - Python Programming for Finance p.20

-

Strategizing - Python Programming for Finance p.21

-

Finding more Alpha Factors - Python Programming for Finance p.22

-

Combining Alpha Factors - Python Programming for Finance p.23

-

Portfolio Optimization - Python Programming for Finance p.24

-

Zipline Local Installation for backtesting - Python Programming for Finance p.25

-

Zipline backtest visualization - Python Programming for Finance p.26

-

Custom Data with Zipline Local - Python Programming for Finance p.27

-

Custom Markets Trading Calendar with Zipline (Bitcoin/cryptocurrency example) - Python Programming for Finance p.28