Data Manipulation

import datetime

import pandas as pd

import pandas.io.data

from pandas import Series, DataFrame

import matplotlib.pyplot as plt

import matplotlib as mpl

import matplotlib.ticker as mticker

import matplotlib.dates as mdates

from matplotlib import style

import numpy as np

style.use('ggplot')

def modifyDataSet():

df = pd.read_csv('X:/stocks_sentdex.csv')

df['time'] = pd.to_datetime(df['time'],unit='s')

df = df.set_index('time')

del df['id']

print df.head()

df.to_csv('X:/stocks_sentdex_dates_full.csv')

def macro():

sp500 = pd.io.data.get_data_yahoo('%5EGSPC',

start=datetime.datetime(2012, 10, 15),

end=datetime.datetime(2014, 5, 11))

ignoreList = ['btcusd','btceur','ltcusd','ltcbtc','btccad','btccny','btcaud','btcjpy','btcgbp']

df = pd.read_csv('X:/stocks_sentdex_dates_full.csv', index_col='time', parse_dates=True)

print df.head()

# we can use this to exclude values, or include specific values.

# you can use this to create indexes, which we will look into later.

for x in ignoreList:

df = df[df.type != x]

counts = df['type'].value_counts()

print counts

_20000MA = pd.rolling_mean(df['value'], 20000)

fixed_20K = _20000MA.copy()

std_1year = pd.rolling_std(_20000MA, 20000, min_periods=20)

ax1 = plt.subplot(2, 1, 1)

sp500['Adj Close'].plot(label='S&P 500')

ax2 = plt.subplot(2, 1, 2, sharex = ax1)

_20000MA.plot(label='20K MA')

plt.legend()

plt.show()

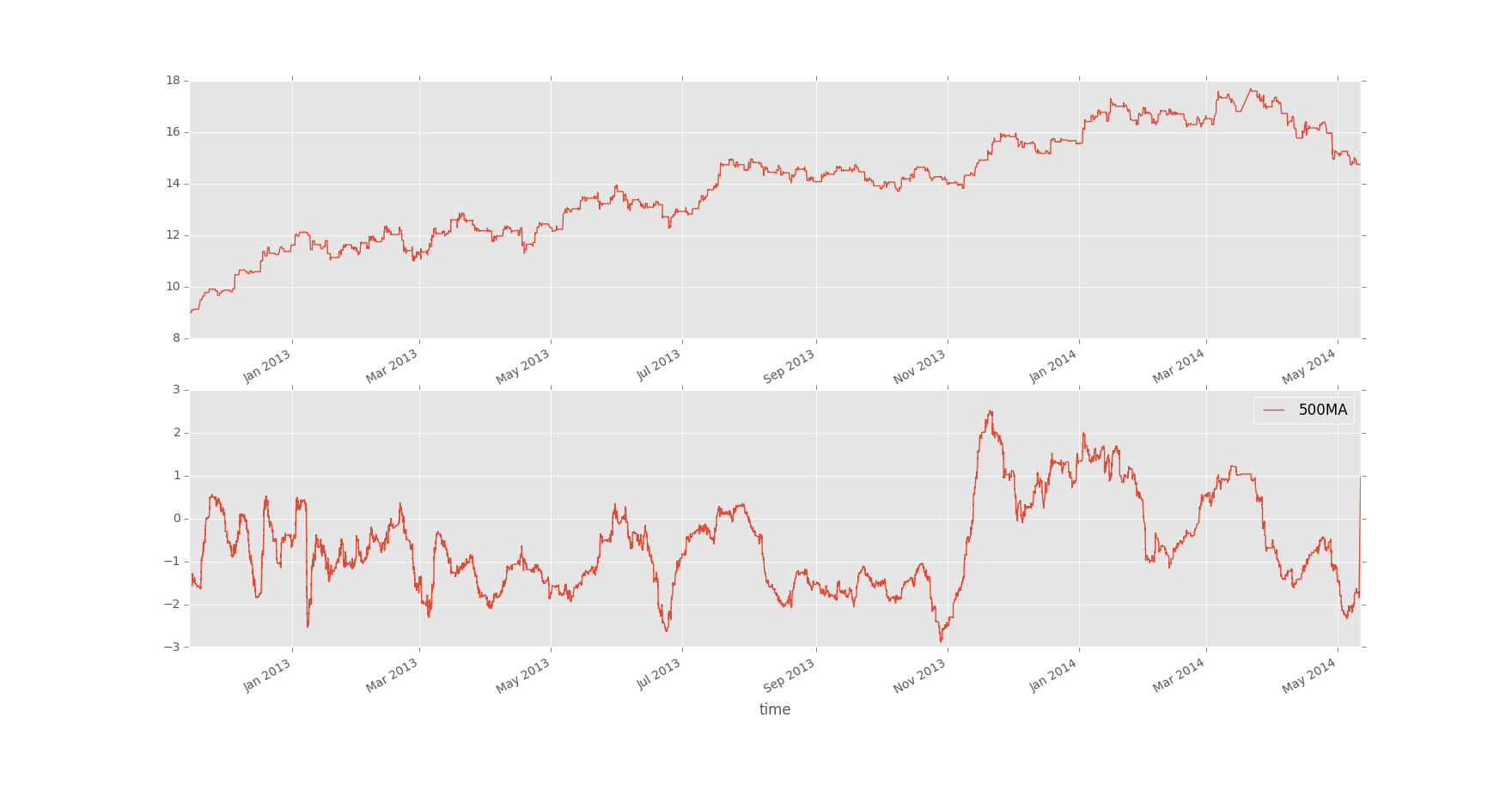

def single_stock(stock_name):

ignoreList = ['btcusd','btceur','ltcusd','ltcbtc','btccad','btccny','btcaud','btcjpy','btcgbp']

df = pd.read_csv('X:/stocks_sentdex_dates_full.csv', index_col='time', parse_dates=True)

print df.head()

for x in ignoreList:

df = df[df.type == stock_name.lower()]

_500MA = pd.rolling_mean(df['value'], 500)

ax1 = plt.subplot(2, 1, 1)

df['close'].plot(label='Price')

ax2 = plt.subplot(2, 1, 2, sharex = ax1)

_500MA.plot(label='500MA')

plt.legend()

plt.show()

single_stock('bac')

The next tutorial: