Resampling - p.9 Data Analysis with Python and Pandas Tutorial

Welcome to another data analysis with Python and Pandas tutorial. In this tutorial, we're going to be talking about smoothing out data by removing noise. There are two main methods to do this. The most popular method used is what is called resampling, though it might take many other names. This is where we have some data that is sampled at a certain rate. For us, we have the Housing Price Index sampled at a one-month rate, but we could sample the HPI every week, every day, every minute, or more, but we could also resample at every year, every 10 years, and so on.

Another environment where resampling almost always occurs is with stock prices, for example. Stock prices are intra-second. What winds up happening though, is usually stock prices are resampled to minute data at the lowest for free data. You can buy access to live data, however. On a long-term scale, usually the data will be sampled daily, or even every 3-5 days. This is often done to keep the size of the data being transferred low. For example, over the course of, say, one year, intra-second data is usually in the multiples of gigabytes, and transferring all of that at once is unreasonable and people would be waiting minutes or hours for pages to load.

Using our current data, which is currently sampled at once a month, how might we sample it instead to once every 6 months, or 2 years? Try to think about how you might personally write a function that might perform that task, it's a fairly challenging one, but it can be done. That said, it's a fairly computationally inefficient job, but Pandas has our backs and does it very fast. Let's see. Our starting script right now:

import Quandl

import pandas as pd

import pickle

import matplotlib.pyplot as plt

from matplotlib import style

style.use('fivethirtyeight')

# Not necessary, I just do this so I do not show my API key.

api_key = open('quandlapikey.txt','r').read()

def state_list():

fiddy_states = pd.read_html('https://simple.wikipedia.org/wiki/List_of_U.S._states')

return fiddy_states[0][0][1:]

def grab_initial_state_data():

states = state_list()

main_df = pd.DataFrame()

for abbv in states:

query = "FMAC/HPI_"+str(abbv)

df = Quandl.get(query, authtoken=api_key)

print(query)

df[abbv] = (df[abbv]-df[abbv][0]) / df[abbv][0] * 100.0

print(df.head())

if main_df.empty:

main_df = df

else:

main_df = main_df.join(df)

pickle_out = open('fiddy_states3.pickle','wb')

pickle.dump(main_df, pickle_out)

pickle_out.close()

def HPI_Benchmark():

df = Quandl.get("FMAC/HPI_USA", authtoken=api_key)

df["United States"] = (df["United States"]-df["United States"][0]) / df["United States"][0] * 100.0

return df

fig = plt.figure()

ax1 = plt.subplot2grid((1,1), (0,0))

HPI_data = pd.read_pickle('fiddy_states3.pickle')

HPI_State_Correlation = HPI_data.corr()

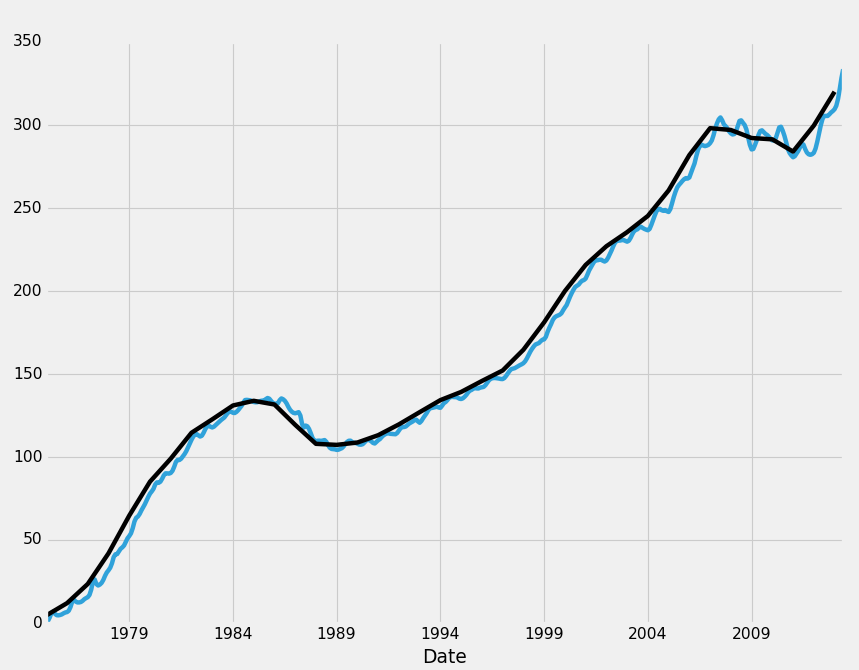

First, let's make this a bit more basic, and just reference the Texas information first, but also resample it:

TX1yr = HPI_data['TX'].resample('A')

print(TX1yr.head())

Output:

Date 1975-12-31 4.559105 1976-12-31 11.954152 1977-12-31 23.518179 1978-12-31 41.978042 1979-12-31 64.700665 Freq: A-DEC, Name: TX, dtype: float64

We resampled with the "A," which resamples annually (year-end). You can find all of the resample options here: http://pandas.pydata.org/pandas-docs/stable/timeseries.html#offset-aliases, but here are the current ones as of my writing this tutorial:

Resample rule: xL for milliseconds xMin for minutes xD for Days Alias Description B business day frequency C custom business day frequency (experimental) D calendar day frequency W weekly frequency M month end frequency BM business month end frequency CBM custom business month end frequency MS month start frequency BMS business month start frequency CBMS custom business month start frequency Q quarter end frequency BQ business quarter endfrequency QS quarter start frequency BQS business quarter start frequency A year end frequency BA business year end frequency AS year start frequency BAS business year start frequency BH business hour frequency H hourly frequency T minutely frequency S secondly frequency L milliseonds U microseconds N nanoseconds How: mean, sum, ohlc

Now we can compare the two data sets:

HPI_data['TX'].plot(ax=ax1) TX1yr.plot(color='k',ax=ax1) plt.legend().remove() plt.show()

As you can see, moving from monthly to annual data has not really hidden anything from us regarding the trend line itself, but one interesting thing to note, however, at least here for Texas, do you think those wiggles in the monthly data look a bit patterned? I do. You can hover your mouse over all the peaks, and start looking at the month out of the year that these peaks are occuring. Most of the peaks are occuring around 6 months in, with just about every low occuring around December. A lot of states have this pattern, and it comes through in the US HPI. Maybe we will just play those trends and be done with the entire tutorial! We are now experts!

Okay not really, I guess we'll continue on with the tutorial. So with resampling, we can choose the interval, as well as "how" we wish to resample. The default is by mean, but there's also a sum of that period. If we resampled by year, with how=sum, then the return would be a sum of all the HPI values in that 1 year. Finally, there's OHLC, which is open high low and close. This returns the starting value, the highest value, the lowest value, and the last value in that period.

I think we're better off sticking with the monthly data, but resampling is definitely worth covering in any Pandas tutorial. Now, you may be wondering why we made a new dataframe for the resampling rather than just adding it to our existing dataframe. The reason for this is it would have created a large amount of NaN data. Sometimes, even just the original resampling will contain NaN data, especially if your data is not updated by uniform intervals. Handling missing data is a major topic, but we'll attempt to cover it broadly in the next tutorial, both with the philosophy of handling missing data as well as how to handle your choices via your program.

There exists 1 challenge(s) for this tutorial. for access to these, video downloads, and no ads.

-

Data Analysis with Python and Pandas Tutorial Introduction

-

Pandas Basics - p.2 Data Analysis with Python and Pandas Tutorial

-

IO Basics - p.3 Data Analysis with Python and Pandas Tutorial

-

Building dataset - p.4 Data Analysis with Python and Pandas Tutorial

-

Concatenating and Appending dataframes - p.5 Data Analysis with Python and Pandas Tutorial

-

Joining and Merging Dataframes - p.6 Data Analysis with Python and Pandas Tutorial

-

Pickling - p.7 Data Analysis with Python and Pandas Tutorial

-

Percent Change and Correlation Tables - p.8 Data Analysis with Python and Pandas Tutorial

-

Resampling - p.9 Data Analysis with Python and Pandas Tutorial

-

Handling Missing Data - p.10 Data Analysis with Python and Pandas Tutorial

-

Rolling statistics - p.11 Data Analysis with Python and Pandas Tutorial

-

Applying Comparison Operators to DataFrame - p.12 Data Analysis with Python and Pandas Tutorial

-

Joining 30 year mortgage rate - p.13 Data Analysis with Python and Pandas Tutorial

-

Adding other economic indicators - p.14 Data Analysis with Python and Pandas Tutorial

-

Rolling Apply and Mapping Functions - p.15 Data Analysis with Python and Pandas Tutorial

-

Scikit Learn Incorporation - p.16 Data Analysis with Python and Pandas Tutorial